When the question comes up

After a severe fire, the immediate concern is always physical safety rather than long-term planning. You must first establish if the house is structurally sound enough to enter. Once that is confirmed, the fire damage rebuild decision becomes a very real calculation.

We constantly guide homeowners through this specific crossroad.

The final choice usually hinges on structural condition, current construction costs, and your insurance limits. Many people immediately wonder if a house fire is repairable at all.

Our team at Seattle Water Damage Restoration will break down the evaluation process right now. Let’s look at the data and explore a few practical ways to respond.

Structural assessment first

A licensed structural engineer must evaluate the home before you make any choices about rebuilding or restoring. This inspection determines exactly what materials are salvageable and what components must be completely replaced.

Our inspectors follow the ANSI/IICRC S700 Standard for Professional Fire and Smoke Damage Restoration, which was formally published in 2025. This authoritative guideline sets the industry baseline for assessing the intensity of fire impacts. A proper evaluation looks at several critical zones.

- Foundation and Footings: Concrete can crack or spall under extreme heat.

- Framing Integrity: Inspectors check for charred load-bearing members and weakened metal connections.

- Roof Structure: Trusses and joists often sustain heavy damage from upward heat travel.

- HVAC and Systems: Acidic soot easily contaminates ductwork and destroys delicate electrical wiring.

The final output is a detailed structural report. Significant damage to the core framing usually makes a complete tear-down the only viable option. Minor damage means a targeted restoration is highly likely.

Common outcomes

Most house fires result in a localized restoration rather than a complete demolition. The exact outcome depends entirely on the spread of the flames and the volume of water used to extinguish them.

We typically classify residential fire incidents into three distinct categories.

Mostly restorable

Most house fires actually fall directly into this category. The flames are usually contained to just one or two rooms, leaving the surrounding structure perfectly sound.

Our restoration crews can confidently return these homes to their pre-loss condition. The process involves structural repairs where needed, comprehensive smoke remediation, and full reconstruction of the burned areas. You also have to factor in contents cleaning.

Typical 2026 US Metrics for Minor to Moderate Fires:

- Average Cost: $3,000 to $50,000 depending on the affected rooms.

- Per Square Foot: Remediation alone averages $4 to $7 per square foot.

- Timeline: 2 to 6 months.

- Insurance: Mostly or completely covered by standard policies.

Significant damage, restorable

A larger fire affects multiple rooms or damages significant structural members. The building shell can still be saved, making the fire damage restore vs rebuild choice lean heavily in favor of restoration.

We handle these intensive projects by executing extensive demolition before any rebuilding starts. This requires complete soot and smoke remediation throughout the entire property, followed by major reconstruction.

Typical 2026 US Metrics for Severe Restorable Fires:

- Average Cost: $50,000 to $150,000 or more.

- Coverage: Generally covered if it stays within your Coverage A policy limits.

- Timeline: 4 to 9 months.

Tear down and rebuild

Severe foundation compromise or massive framing loss means restoration is no longer safe or practical. The existing home is completely demolished, and a new structure is built from the ground up.

Our project managers see this happen when the fire burns extremely hot for a long duration. The process requires full site clearing, debris removal, and securing new construction permits.

Typical 2026 US Metrics for Rebuilding:

- Average Cost: $150 to $300 per square foot across most US markets, reaching up to $500 for luxury custom homes.

- Insurance Limit: Your carrier pays up to the Coverage A limit, making any overages an out-of-pocket expense.

- Timeline: 12 to 18 months for permitting, demolition, and the new build.

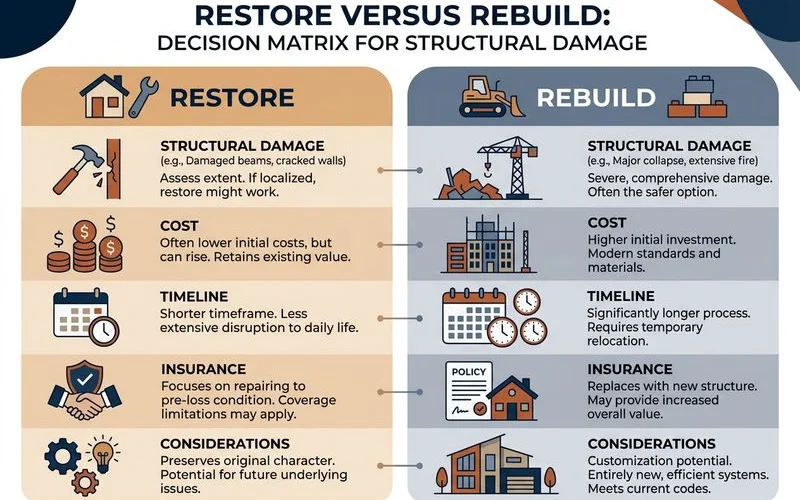

When restoration usually wins

Restoration is usually the best choice when the structural damage is contained to less than 40% of the building. It is also the smartest financial move if your insurance payout will not cover current new-construction rates.

We frequently recommend restoration for older homes with unique architectural character. Preserving vintage hardwood, custom plaster, or period details is something new construction simply cannot replicate.

Here are the most common reasons homeowners choose to restore:

- Faster Timelines: Restoration is almost always several months faster than a full rebuild.

- Budget Constraints: Rebuilding a 2,000 square foot home can easily exceed $400,000 today, which often surpasses standard policy limits.

- Zoning Grandfathering: Rebuilding sometimes forces you to comply with strict new local zoning laws, while restoration often bypasses these hurdles.

- Sentimental Value: A strong emotional attachment to the existing home makes saving it a top priority.

When rebuilding usually wins

Rebuilding is the mandatory choice when a fire destroys the foundation or compromises the primary load-bearing architecture. It also makes sense if you have a modern, generic home that is relatively inexpensive to replace.

Our team often points out that a total loss is a chance to fix preexisting layout problems. If your insurance policy features full replacement cost coverage that easily handles 2026 construction prices, starting fresh is highly appealing.

Consider these factors that favor new construction:

- Severe Structural Compromise: Safety risks make restoration impossible.

- Outdated Floor Plans: You can finally design the layout you actually want.

- Favorable Insurance Limits: Your Coverage A limit easily exceeds the $150 to $300 per square foot rebuild cost.

- Hidden Contamination: Extensive water damage from firefighting efforts can cause deep mold issues, making a clean slate much safer.

The insurance dimension

For most partial losses, insurance companies pay the exact cost of restoration to bring the property back to its pre-loss condition. They will not fund a completely new build if a safe repair is financially feasible.

We work closely with carriers to ensure every detail is documented accurately. For total or near-total losses, the insurer may pay out the Coverage A limit and let you decide how to proceed.

The insurance landscape varies wildly depending on your location. Roughly 20 US states, including Florida and Ohio, operate under Valued Policy Laws. In these specific states, if your home is declared a total loss from a covered peril, the insurer must pay the full face value of the policy, regardless of the actual replacement cost.

Our fire damage restoration advocates work with the adjuster on the scope and the final decision. The carrier’s adjuster will categorize your payout using one of two primary valuation methods.

| Valuation Method | How It Works in 2026 | Financial Impact on Rebuilding |

|---|---|---|

| Actual Cash Value (ACV) | Pays the cost to replace the damaged property, minus depreciation for age and wear. | Results in higher out-of-pocket costs for homeowners. |

| Replacement Cost Value (RCV) | Pays the actual current market cost to rebuild or repair with similar materials. | Provides better financial support for a full recovery. |

Sometimes the right financial answer is restoration, sometimes it is a rebuild, and occasionally a hybrid approach works best.

The personal factor

Cost and structural integrity are not the only inputs in this massive decision. For many families, the emotional toll of a fire heavily dictates the final path forward.

We fully respect the psychological side of property loss. The desire to preserve a beloved family home often makes restoration the obvious choice, even when a basic rebuild might look cheaper on paper. Conversely, the trauma of a major fire makes some people want to completely start fresh in a new structure.

You must also consider the logistics of your daily life.

- Community Ties: Keeping kids in the same school district pushes families to stay on the existing lot.

- Interest Rates: Giving up an old, low mortgage rate to finance a brand-new build in the 2026 market is a major financial hurdle.

- Time Displacement: Living in a temporary rental for 18 months during a rebuild is exhausting compared to a 4-month restoration.

Our team is not here to judge those personal decisions. Providing clear information is our only goal, allowing you to understand what is possible and what each option entails. We then work tirelessly with whatever you decide.

What to do this week

If you are facing this decision right now, your immediate focus should be gathering hard data. You cannot make an informed choice until you have accurate numbers from certified professionals.

We recommend pausing any major commitments until you secure a few key documents. The decision does not have to be finalized in the first week.

Take these concrete steps over the next few days:

- Get a formal structural assessment from an engineer.

- Request a restoration estimate from a licensed remediation company.

- Obtain a new-construction estimate for a home of comparable size and quality.

- Get your insurance adjuster’s preliminary scope of work in writing.

- Check if your state operates under a Valued Policy Law for total losses.

Most homeowners end up proceeding with restoration, and the vast majority are glad they did. The right answer depends entirely on your specific situation. Take the time to build an informed strategy, and you will secure the best possible outcome for your property.

Frequently Asked Questions

Who decides restore vs rebuild?

Is rebuilding always more expensive than restoring?

Will insurance pay for rebuild vs restore?

Related Guides

Can Fire-Damaged Belongings Be Restored?

Many fire-damaged contents can be saved. What's salvageable, what's not, and the restoration process.

Smoke Odor and Soot Removal: How It Works

Soot removal and smoke-odor elimination — thermal fog, hydroxyl, and ozone explained.

What to Do After a House Fire

After the fire department leaves, what's next? Safety, documentation, immediate calls, and the fire restoration process.

Learn more about Fire & Smoke Damage Restoration

Talk to a real local dispatcher 24/7. Certified technicians on-site in 60 minutes — direct insurance billing.