We hear panicked homeowners ask, does insurance cover mold, during sudden water emergencies every week. Right now, recent 2026 housing statistics show 47% of U.S. homes experience visible mold or odors.

An unexpected indoor storm from a burst pipe turns into a massive fungal headache quickly. Our restoration crews know that understanding the rules beforehand is your best defense.

Let’s look at what the policies actually say and map out exactly how to handle a claim.

The coverage question depends on the cause

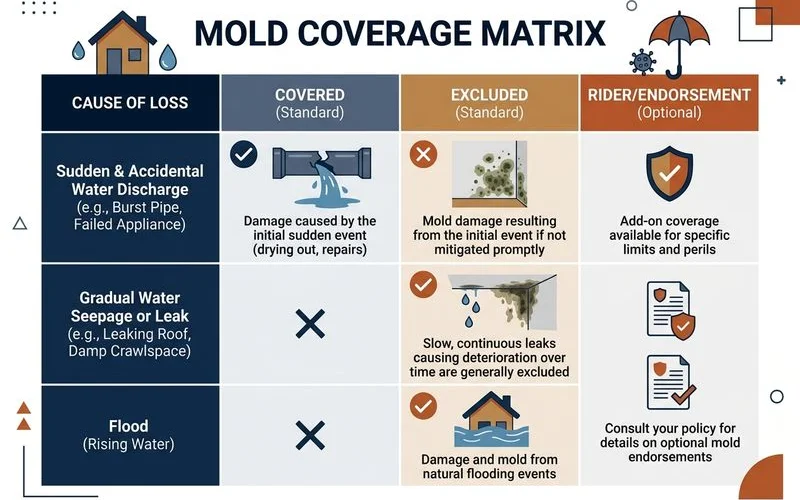

Mold insurance coverage relies entirely on the exact event that brought water into your home. The same fungal growth might be fully paid for or completely excluded based on your policy language and adjuster documentation. We have found that the source of the moisture is the single deciding factor.

According to 2026 real estate data, a property’s resale value can drop by up to 37% if these situations are mishandled. Our experts always trace the moisture back to its origin before calling an adjuster. This targeted approach prevents instant denials from insurance companies.

What’s typically covered

Standard HO-3 policies cover mold removal only when it results from a sudden, accidental, and covered water event. Burst pipes or severe storm-driven roof leaks usually trigger this protection. We secure approvals for clients daily when the timeline is clear and immediate.

When asking if is mold remediation covered, standard policies provide strict limits. Basic insurance plans across the U.S. typically cap mold payouts at just $5,000 to $10,000. Our billing department regularly sees basement or whole-house projects easily exceed the $10,000 mark. This discrepancy means you must maximize the allowable funds properly.

- Sudden plumbing supply line failures.

- Appliance water line bursts.

- Wind-driven rain entering a newly damaged roof.

- Accidental fire suppression water damage.

What’s typically excluded

Insurers routinely deny claims linked to gradual issues like slow leaks, high humidity, or delayed maintenance. Your policy expects you to catch and fix minor dampness before it becomes a major fungal colony. We tell clients that condensation-driven growth in attics is almost never covered.

Another major exclusion is flooding from groundwater or overflowing rivers. Our mitigation teams see many homeowners assume standard insurance covers floodwater damage. You need a separate National Flood Insurance Program policy to handle ground-level water intrusion.

Insurers look for rust, rot, or long-standing water marks as definitive proof to deny your claim.

Mold endorsements (riders)

Adding a specific mold endorsement to your insurance explicitly increases your payout limits for fungal removal. This is a separate rider that modifies your standard HO-3 agreement. We strongly recommend this upgrade for anyone in vulnerable or humid areas.

A standard mold rider in the U.S. currently adds roughly $50 to $150 to your annual premium. Our clients who carry these riders often enjoy coverage caps expanded to $25,000 or even $50,000. It is a minor upfront cost that prevents catastrophic out-of-pocket expenses later.

| Policy Type | Typical Annual Added Cost | Maximum Coverage Limit | Coverage Trigger |

|---|---|---|---|

| Standard HO-3 | $0 (Included) | $5,000 to $10,000 | Sudden, covered peril only |

| Mold Endorsement | $50 to $150 | $25,000 to $50,000 | Sudden, covered peril only |

| Water Backup Rider | Varies by carrier | Matches endorsement | Sump pump or sewer failure |

How to document a claim

Thorough documentation is the single factor that pushes a pending claim into an approved status. Vague phone calls to an adjuster will almost certainly result in a low-ball offer or flat denial. We build an evidentiary file for every property before any demolition begins.

The U.S. federal government recently mandated the ANSI/IICRC S520-2024 standard for all military housing in the 2026 National Defense Authorization Act. Our crews strictly follow this exact gold-standard framework for professional mold remediation in your home. This level of rigor leaves the insurance adjuster with zero room to argue against the required scope of work.

To guarantee a fair review, follow these strict documentation steps:

- Photograph the visible growth and the precise water source immediately.

- Record the exact date and time you discovered the sudden water event.

- Hire a certified inspector to capture objective moisture readings.

- Submit the cause of loss clearly to emphasize the sudden nature of the event.

- Save every receipt, daily drying log, and third-party laboratory report.

Common claim mistakes

Certain missteps during the filing process will automatically trigger an adjuster to reject your request. A few wrong words or delayed actions can void your protection entirely. We actively guide homeowners away from these frequent traps.

Reporting the Damage Too Late

Most insurance policies demand prompt notification following a water disaster. Waiting weeks to mention the fuzzy growth makes the damage look like a gradual maintenance failure. Our dispatchers advise calling your carrier the exact same day you discover the burst pipe.

Mixing Covered and Uncovered Scope

Combining a sudden disaster claim with an old home improvement project is a terrible idea. Adjusters scrutinize estimates heavily to find unapproved upgrade requests. We separate the emergency stabilization completely from any preexisting ventilation issues in the attic.

- Keep emergency water extraction separate from remodels.

- Never bill routine maintenance to an active claim.

- Document the exact boundary of the sudden damage.

Characterizing the Cause Poorly

Using phrases like long-running leak or ongoing dampness on a recorded line will ruin your chances. Insurers listen for keywords that suggest owner negligence. Our project managers advise clients to stick to factual, precise terms like sudden pipe failure.

Skipping Professional Remediation

Attempting DIY cleanup with bleach and a sponge rarely satisfies an insurance carrier’s requirements. Stachybotrys chartarum, commonly known as black mold, forces professional contractors to increase rates by 15% to 25% due to mandated safety protocols like full-face respirators and HEPA scrubbers. We provide the rigorous, documented removal that adjusters expect before releasing funds.

When to file vs. when not to

Paying for the cleanup out of pocket is sometimes smarter than reporting it to your insurance carrier. Filing a claim automatically goes on your permanent property record, regardless of the payout. We help homeowners run the math before they make that binding phone call.

The national average for a standard removal project is currently around $2,368. If your insurance deductible is $2,000, you will gain almost no financial benefit from filing a claim. Our estimators will honestly tell you if a minor bathroom job should just be handled privately to protect your premium rates.

What we handle

Our team manages the entire technical recovery and insurance billing process so you can focus on your family. Removing the back-and-forth negotiation with the carrier drastically reduces your stress. We align the final scope directly with the adjuster using irrefutable industry standards.

For the professional mold remediation projects we accept, we handle everything from the initial moisture mapping to the final clearance testing. Most of our clients end up paying only their baseline deductible. We secure your property, protect your health, and ensure the final restoration lasts for decades.

If you are still wondering, does insurance cover mold, our estimators are ready to evaluate your exact situation.

- Professional moisture mapping and thermal imaging.

- Direct insurance carrier billing and documentation.

- Verified clearance testing by third-party laboratories.

- Complete structural drying and sanitization.

Frequently Asked Questions

Is mold ever covered without a rider?

What's a mold rider worth?

How do I document a mold claim properly?

Related Guides

Attic Mold Removal in the Pacific Northwest

Why PNW attics get mold and what proper remediation looks like — ventilation, sheathing, and root-cause fixes.

Basement and Crawl Space Mold Removal

Below-grade mold in PNW homes — sources, removal process, and why source fix matters.

Is Black Mold Dangerous? Health Risks Explained

Stachybotrys (so-called black mold) and the real health risks — what's myth, what's evidence-based, and when to call professional remediation.

The IICRC S520 Mold Remediation Process Explained

Step by step through the IICRC S520 mold remediation standard — what professional remediation actually involves.

Learn more about Mold Remediation

Talk to a real local dispatcher 24/7. Certified technicians on-site in 60 minutes — direct insurance billing.