The short version: Does homeowners insurance cover water damage?

We regularly hear panicked homeowners ask, does homeowners insurance cover water damage, while water is actively pooling on their living room floor.

That initial shock quickly turns into a stressful guessing game about your financial exposure. Homeowners insurance usually protects you from sudden plumbing disasters, but it strictly excludes gradual leaks and neglect.

The fine line between those two categories dictates whether your claim is approved or denied.

Our restoration teams spend every day working through these exact policy boundaries with local adjusters. This guide will break down exactly what standard policies protect, where the hidden gaps lie, and how to properly document your loss.

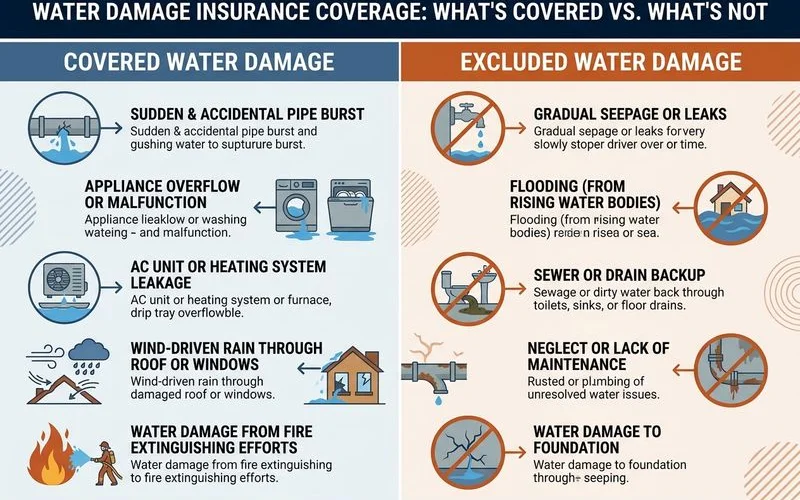

What’s typically covered

Standard HO-3 homeowners policies act as a financial safety net for sudden and accidental plumbing disasters. This includes chaotic incidents like a ruptured main supply line or a washing machine hose that bursts without warning.

We find that gaining absolute clarity on your specific coverage areas saves significant frustration during an emergency. The average plumbing deficiency inherited by a buyer leads to a $5,800 water damage claim in the US, according to 2025 inspection data.

A covered event usually triggers three very different types of payouts under your standard agreement. Our crews prioritize mapping out exactly which of these policy buckets applies to your situation. This organized approach prevents confusion when the adjuster arrives on site.

| Policy Section | What It Pays For | Typical 2026 Limits |

|---|---|---|

| Coverage A (Dwelling) | Structural repairs to drywall, flooring, and framing. | Up to your total property policy limit. |

| Coverage C (Contents) | Damaged personal belongings, electronics, and furniture. | Usually 50% to 70% of your Dwelling limit. |

| ALE (Loss of Use) | Hotel stays and meals if you must be displaced. | Usually 20% of your Dwelling limit. |

Specific Covered Scenarios

When you are wondering, is water damage covered, know that insurance carriers look for specific trigger events to authorize a payout. This strict criteria separates a valid emergency from a routine maintenance issue.

- Burst pipes: Supply lines, fittings, or water heaters that fail without warning.

- Sudden plumbing leaks: A brass fitting that lets go or a discharge line that aggressively disconnects.

- Appliance failures: Washing machines, dishwashers, and refrigerators with active ice makers.

- Storm-driven roof leaks: Situations where the storm physically damaged the roof structure and water entered.

- Frozen pipes that burst: Provided you maintained a reasonable heat level inside the property.

What’s typically excluded

Flood Damage and Ground Saturation

The National Flood Insurance Program manages most flood protection policies across the country. Standard home insurance never covers water that enters from outside, such as storm surges, heavy river overflow, or ground saturation.

We watched this devastating coverage gap play out during the severe December 2025 storms that struck King and Snohomish counties. That specific event prompted a major FEMA disaster declaration (FEMA 4906-DR-WA), leaving unprotected residents to fund their own rebuilding efforts.

An active NFIP policy caps payouts at $250,000 for your physical building and $100,000 for your personal contents in 2026. You must secure this separate federal coverage immediately if your property sits in a designated high-risk zone.

Sewer and Drain Backups

Standard property policies also exclude dirty water that reverses direction and enters through municipal sewer lines or basement sump pumps. The EPA estimates that roughly 75,000 sewage backups occur across the United States every single year.

Our technicians classify this highly contaminated sludge as Category 3 water, which requires aggressive biohazard removal protocols. Professional sanitization for a severe backup frequently costs between $2,000 and $10,000 out of pocket.

A simple sewer backup rider completely changes this financial equation and forces the carrier to pay for the cleanup.

Gradual Damage and Neglected Maintenance

Slow plumbing leaks and deteriorated shower caulking fall entirely on the homeowner to monitor and repair. Insurance carriers fully expect you to perform routine maintenance on your pipes and replace worn fixtures before they fail.

We often see claims aggressively rejected because a field adjuster spots extensive dry rot, proving the leak existed for several months. Mold removal is occasionally approved if it results directly from a sudden, covered pipe burst.

Most national providers strictly cap that specific mold remediation payout at a maximum of $5,000 to $10,000.

Documentation that helps your claim

Your immediate actions during the first few hours of a flooded basement directly impact your final settlement offer. Desk adjusters rely heavily on your initial visual evidence to determine if a pipe failure was truly sudden and accidental.

We tell every single client to start capturing high-resolution photos and wide-angle videos before anyone touches the mess. Timestamped digital media from a modern smartphone locks in the exact GPS coordinates and time of the incident.

This digital footprint proves the timeline of the failure to your skeptical carrier. Moving too fast to extract the water can accidentally erase the specific proof you need for approval.

Evidence That Strengthens Your Case

- Capturing wide-angle video: Show the standing water, the active source, and the full extent of the damage before extraction begins.

- Saving physical evidence: Keep the specific broken brass fitting or burst pipe to show the field adjuster.

- Acquiring professional documentation: Request a detailed emergency mitigation invoice from a fully licensed restoration professional.

- Using precise metadata: Rely on your smartphone camera to lock in the exact time and GPS location of the disaster.

Mistakes That Hurt Your Payout

- Discarding broken parts: Tossing out the damaged plumbing components before the official adjuster arrives on site.

- Waiting to file: Delaying your initial phone call to the insurance carrier by several days.

- Attempting DIY cleanup: Trying to handle complex Category 3 biohazard water extraction yourself.

- Combining damages: Mixing old wear-and-tear issues into a brand new emergency claim report.

How direct insurance billing works

Handling a flooded property is stressful enough without having to float a massive construction bill on your personal credit card. Direct insurance billing removes that heavy burden by keeping the primary financial transaction strictly between the restoration contractor and the carrier.

Our administrative staff works exclusively with your assigned adjuster inside Verisk’s Xactimate software to standardize the pricing. This specific industry software ensures complete transparency and prevents arguments over individual line items.

You simply pay your standard deductible amount, and the insurance carrier directly funds the rest of the approved project.

| Step | Traditional Reimbursement | Direct Insurance Billing |

|---|---|---|

| Out-of-Pocket | You pay the full mitigation invoice upfront. | You only pay your set policy deductible. |

| Pricing Validation | You argue over line items with the carrier. | Contractor uses standard Xactimate pricing. |

| Final Payment | You wait weeks for a reimbursement check. | The carrier pays the contractor directly. |

For active emergencies that need mitigation right now, call our emergency restoration dispatch immediately. We will start the professional documentation process on site while you are still figuring out the paperwork side.

This rapid response safely protects your property and secures the structural evidence required for a solid claim.

Coverage gaps to fix before you need them

Reviewing your specific declarations page right now is the cheapest property protection you can buy. Adding targeted endorsements costs just pennies compared to funding a massive kitchen reconstruction project out of your own savings.

Our field managers highly recommend talking to your local agent about four crucial upgrades before the next storm system hits. Securing these specific riders guarantees your water damage insurance coverage is actually protecting your home from the most destructive local hazards.

- Sewer backup endorsement: Costs roughly $50 to $250 annually and provides up to $25,000 in vital Category 3 cleanup coverage.

- Sump pump failure rider: Replaces burned-out mechanical pumps and pays for the resulting lower-level water extraction.

- Mold endorsement: Expands coverage for properties with high-risk basements and crawl spaces where secondary damage happens fast.

- NFIP flood insurance: Essential for properties near overflowing rivers, especially given the history of severe floods across King and Snohomish counties.

A quick ten-minute phone call to your local agent today is infinitely better than a massive, unexpected expense tomorrow. When you finally ask your representative, does homeowners insurance cover water damage, make sure you clarify exactly which special endorsements you have actively attached to your policy.

We want you to have total confidence in your coverage before a disaster ever strikes. This proactive step secures your family’s financial future against unpredictable plumbing failures.

Frequently Asked Questions

Is a burst pipe covered?

Does insurance cover gradual leaks?

Will you bill my insurance directly?

Related Guides

How Long Does Professional Structural Drying Take?

Professional structural drying usually takes 3-5 days. What affects the timeline and how we monitor to the dry standard.

7 Signs of Hidden Water Damage in Your Home

Recognize the early warning signs of water damage behind walls, under floors, and in your crawl space — before it becomes a mold problem.

Water Damage Categories 1, 2, and 3 Explained

IICRC S500 water categories explained: clean, gray, and black water risk levels and when each needs professional Seattle restoration.

How the Water Damage Insurance Claim Process Works

Step by step: from filing the claim to documenting damage, working with the adjuster, and getting paid for water damage restoration.

Need help with water damage?

Talk to a real local dispatcher 24/7. Certified technicians on-site in 60 minutes — direct insurance billing.